Real ranges, not hype, and why “make” is the wrong word.

When people ask how much you can make house hacking, they’re usually picturing a check. That’s the wrong frame, and it leads to disappointment. House hacking rarely hands you a fat monthly profit. What it hands you is a housing cost so low that the savings become the return.

Let me show you what that actually looks like in dollars.

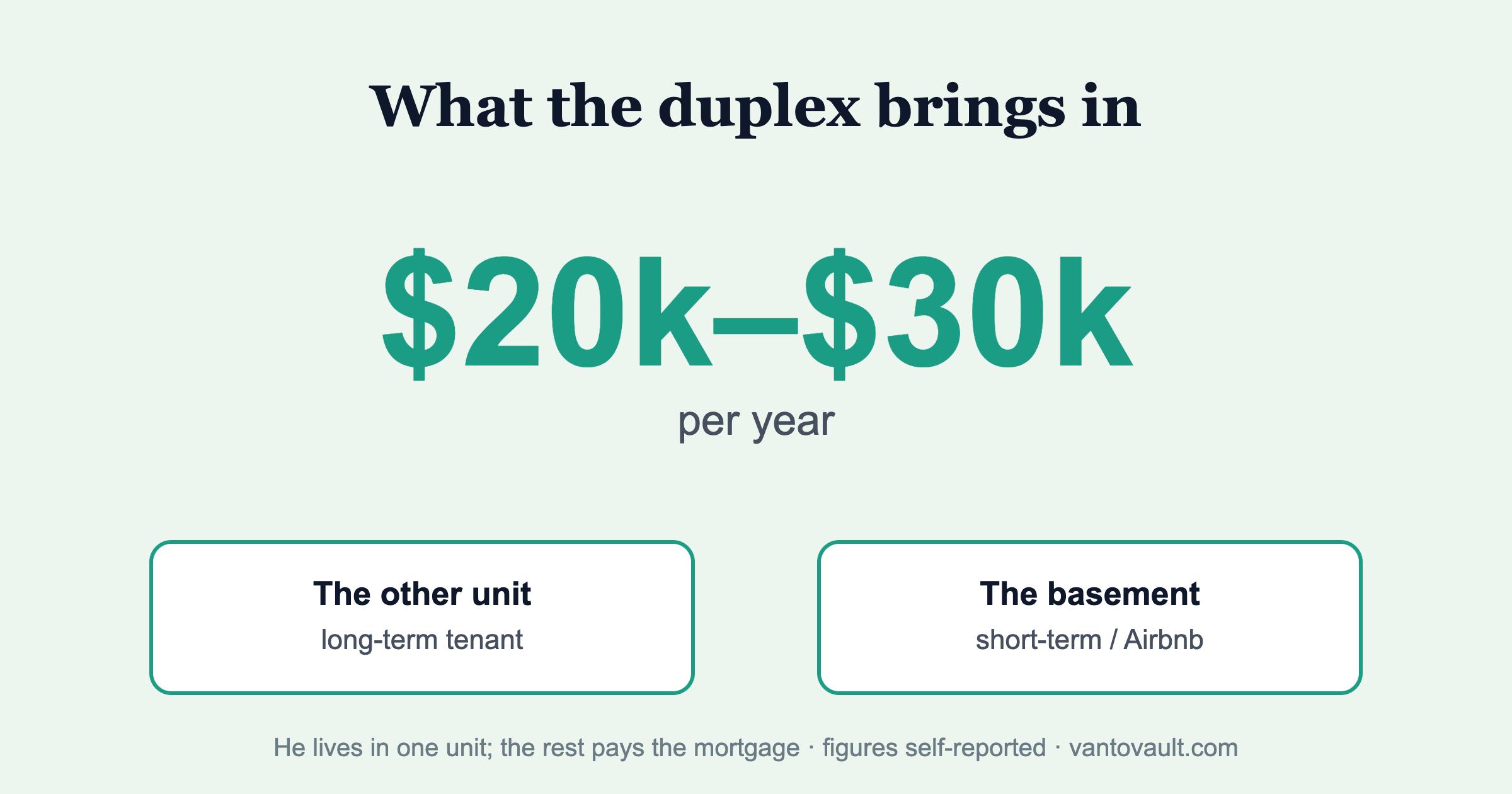

What it “made” me

While I live in my duplex, the building collects about $2,283/month, $1,200 from the upstairs tenant and roughly $1,083 from the basement short-term rental. My total housing payment is about $2,880/month.

So the property doesn’t put cash in my pocket. On paper it runs negative, because I live in one unit rent-free. But my effective housing cost is about $600/month instead of the $1,500 I paid before. That’s a swing of roughly $900 a month, about $10,800 a year — that stays in my budget.

That $10,800 is the real “income.” It just shows up as money I don’t spend rather than money I collect.

The real ranges

What you’ll save depends on your market and layout, but here’s a realistic spread for a small-multi house hack:

- Modest: $300–$500/month off your housing cost. Common in pricier markets or with one rented unit.

- Solid: $600–$1,000/month, where rents cover most of the payment. This is roughly my situation.

- Exceptional: housing cost near zero or below, usually with multiple income streams (a second unit plus a basement or ADU rental).

Then there’s the part you can’t see monthly

The monthly savings is only half the return. The other half is quieter:

- Loan paydown, your tenants are retiring your mortgage balance every month.

- Appreciation, you’re building equity on the whole building, not just your share.

- The move-out flip, when you leave and rent your unit, the property usually turns cash-flow positive on its own.

Add those up over a five-year hold and a house hack that looked unimpressive in year one looks excellent by year five. (The projection tool shows that curve.)

The bottom line

How much can you make house hacking? Probably not much in monthly cash, and a lot in saved rent, paid-down debt, and equity. If you’re chasing a paycheck, you’ll undervalue it. If you’re chasing financial independence, it’s one of the fastest legal accelerants a regular earner has.

Run your numbers and look at the effective housing cost, not the cash flow. That’s where the money actually is.

Curious what a specific deal would save you? Send me the listing.

If you’re new to all this, start with what house hacking is.

The First-Property Bundle

The step-by-step playbook, the six-calculator deal-analyzer toolkit, and the down-payment-assistance finder — the exact system I used to go from a van to a duplex.

Pay what you want. Name your price — and if money’s tight, take it for less.

Get the bundle →Get the free $0-to-First-Property Roadmap

The five-stage plan I used to go from living in a van to owning a duplex, no rich parents required.