Over the past 20 years, I’ve watched my income grow in fits and starts. I’ve had years where a raise came at my annual review—maybe 2-4% if I was lucky. And I’ve had years where my income jumped 15%, 20%, even 49% in a single move.

The difference wasn’t talent, promotions within the same company, or negotiating aggressively for better compensation. It was switching jobs.

This is somewhat controversial advice and still undervalued, although, the job market is changing again. In my experience, for whatever that is worth, it’s crucial to be open to switching jobs/companies if you want to increase your income, develop your career skills, and eventually build wealth. Because inflation doesn’t give a discount for loyalty, staying put for five to ten years often doesn’t help you move ahead.

The Math of Staying Put

Here’s the layout of what often happens when you stay at the same company for five years:

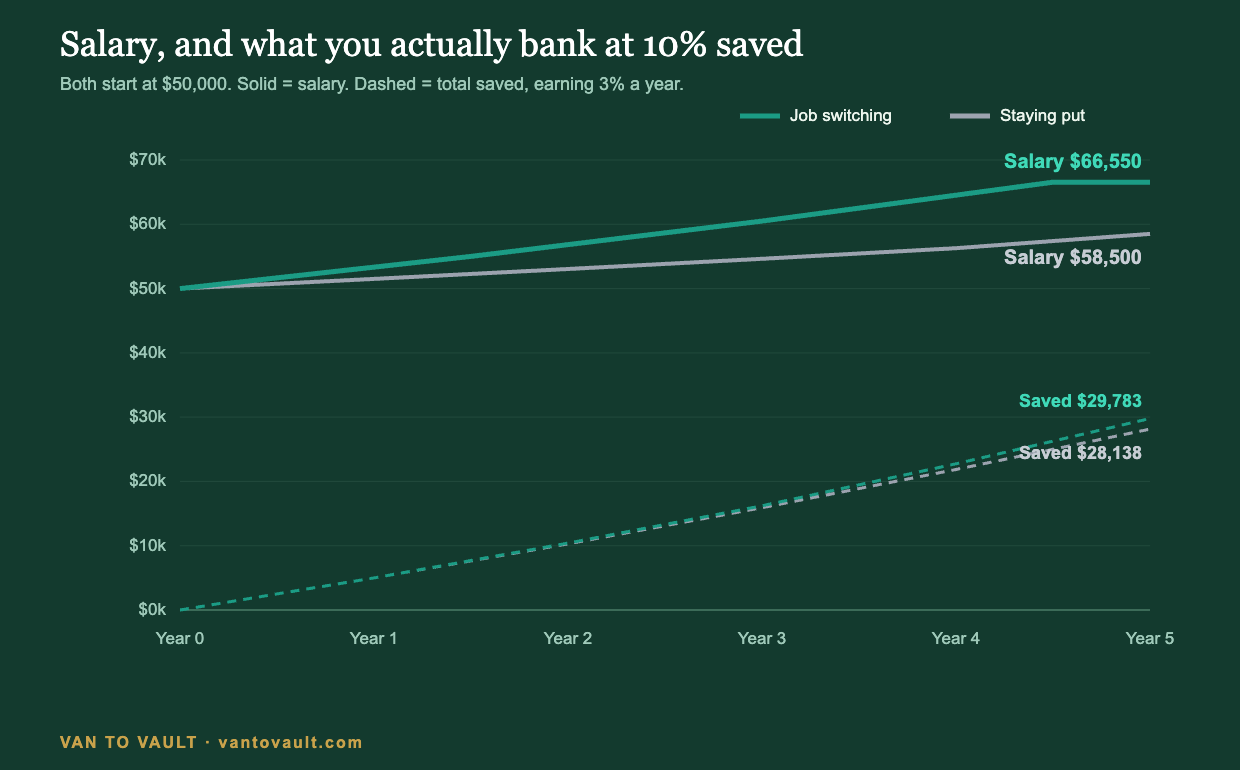

Let’s say you make $50,000 when you start. You get 3% raises for four years straight. Maybe you get 4% in year five as a token acknowledgment that you’re senior now.

After five years, you’re making about $58,500.

Assume inflation runs 2% a year, which is roughly 10% over the five years. That works out to your $58,500 having only about 6% more buying power than your $50,000 did at the start: five years of showing up for a 6% real raise.

Compare that to job switching. Start at $50,000. After 18 months, find a new role. The job market for someone with your specific experience is usually hotter than the internal ladder at your current company. You land a 10% bump to $55,000. Eighteen months later, another move, another 10%, to $60,500. Again eighteen months later, another 10%, to $66,550.

In five years the switcher is earning $66,550, about $8,000 a year more than the person who stayed and roughly a third above where they both started. After the same 2% inflation, that’s still about a 20% real raise, more than three times what staying put delivered.

Now put a real number on it. Say each version of you saves 10% of what you earn and parks it somewhere paying 3% a year. Over the five years, the person who stayed put earns about $265,000 and, with interest, banks about $28,100. The person who switched earns about $282,000 and banks about $29,800. Every raise doesn’t just lift your salary, it lifts how much that same 10% habit sets aside.

Notice the saved amounts are close, only about $1,700 apart. That surprises people, but it follows from the rule: when you save a flat 10% of income and you both started at the same $50,000, the switcher’s bigger paychecks have only been bigger for a year or two, so they barely move the five-year total. It matters even less in real terms: with costs rising about 2% a year and the cash earning 3%, that pile gains only about 1% a year in actual buying power. The real prize isn’t the five-year cash pile. It’s the salary itself. By year five the switcher earns about $8,000 more every year, and that gap compounds. Five years is just where the two lines start to pull apart.

Why Companies Don’t Compensate Internal Moves

There’s this idea that leaving looks bad, that companies reward loyalty. It’s mostly backwards. It also is out-dated, as pensions and well funded 401k plans alongside simpler and better medical plans were part of compensation. In other words, there were a handful of reasons to stay at a company (literally rewarding loyalty by vesting your 401k match, for instance). Some of these still exist, and you should be mindful of them (it may not make sense to leave your employer if they provide a 100% match to your 401k contribution, up to, say 8%, AND cover you and your spouse’s healthcare plan premiums). But, generally speaking, our benefits in the workforce have become complicated, often un-useful, and rarely as good as a defined benefit pension.

Companies have budgets for new hires that don’t apply to current employees. HR has salary bands for positions. If you’re already inside your company’s band for your current role, getting you to the next band usually requires a promotion—and promotions happen on someone else’s timeline, not yours.

When you switch jobs, you’re negotiating a new band. You’re a market rate entry point, not an internal adjustment.

I’ve been on both sides. As an employee, the bump from an external hire was always bigger than what I could get for the same role by staying. As a manager, I couldn’t fight for my existing team the way I could fight for a new headcount budget. It’s not personal. It’s how the system works.

The “Loyalty” Argument Doesn’t Hold

I’m not rejecting all pushback on this. Stability matters. Your specific situation will also dictates whether or not it is worth considering. And sometimes it can be beneficial to have shown you can “stick with something.” Some employers value commitment.

All true. But commitment doesn’t equal staying at one company for your entire career. Does it even mean doing your job well, finishing what you start, and not job-hopping every six months, just to be rewarded with a 2% bump?

Switching every 12-18 months is not flaky. It’s smart career management. Most professional roles take 6-12 months to really hit your stride and contribute meaningfully anyway. By month 18, you’ve learned the systems, built relationships, delivered something. You’re valuable. That’s the moment to leave, while you have the most leverage.

If an employer thinks that’s disloyal, that’s a signal about the employer, not about you. It is also always possible that if they value as much as a competitor might, they’ll offer you the same or more to keep you (which poses its own risks, but is worth considering). If they don’t, why would you stay?

It Gets Harder the Longer You Wait

There’s a real cost to staying too long in one place: your resume gets stale. Your skills can atrophy, as you get locked into the same systems and same tasks.

After three or four years at the same company, hiring managers start asking why you haven’t moved. Not in a hostile way, but it becomes a question. Did you get comfortable? Are you afraid of change? Have you even tried to leave?

Switching every 12-18 months, on the other hand, tells a story: you delivered, you learned, you leveled up, you did it again. You’re reliable. You’re ambitious without being reckless.

Also, the longer you stay in a single company, the more your specific skills and context become hard to translate to an external market. Your technical skills are current. But your salary history, your internal titles, your specific tools—they all become less relevant to what the outside world will pay.

The Compound Effect

Here’s what actually compounds your wealth:

Getting 10% raises a year, every year, starting early in your career. Not waiting for promotions. Not hoping for annual raises. Actively moving to jobs that pay more.

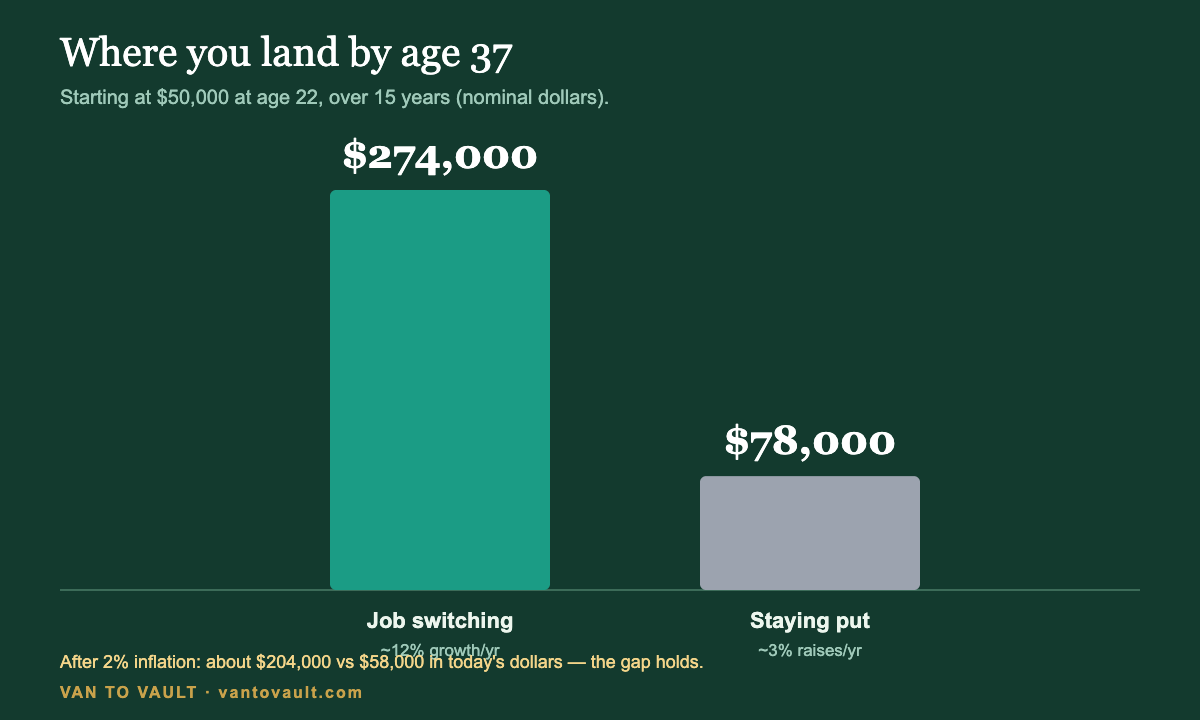

If you start at $50,000 at 22, and over the next 15 years you average 12% salary growth per year through job switching, you’re making about $274,000 by 37. That translates to a real down payment on a house, a strong retirement plan, a healthy savings, and some investments. That’s real capital. That’s something that breaks you out.

If you’d stayed at one company with 3% annual raises, you’d be at about $78,000. Still paying off student loans. Still priced out of the real estate market.

The difference compounds. Even after stripping out 2% inflation, which puts those figures near $204,000 and $58,000 in today’s dollars, the gap between the two barely moves. Every dollar you’re not making at 25 is five years of lost growth, lost investing, lost compounding.

Example three: turning the raises into a duplex

This is the part that actually changed my life, and it’s the path I took.

By year five, the aggressive switcher is earning about $66,550 and has saved about $29,800. That isn’t enough to buy a house outright, and it doesn’t need to be. At 3.5% down, the down payment on a $460,000 duplex is about $16,100. The savings covers the down payment and most of the closing costs, and in my case a county first-time-buyer program covered the rest.

The duplex isn’t only a place to live. The second unit plus an Airbnb basement bring in roughly $20,000 to $30,000 a year. I locked a 4% 30-year fixed rate, which kept the payment near $2,100 a month before taxes and insurance, and the rental income covered most of it, so my real housing cost dropped to a fraction of what renting would have cost. The higher salary from switching mattered as much as the savings here, because lenders count most of that rental income, and a $66,550 salary plus the rental was enough to qualify comfortably where the stay-put salary would have been a stretch. Meanwhile you own a $460,000 asset that pays itself down every month and appreciates while you sleep.

Line up the three people at year five. The one who stayed put has about $28,100 in cash and is still renting. The one who switched has about $29,800 in cash and is in position to buy, but won’t be adding passive income to the mix (or lowering their housing costs, however you’d prefer to look at it. The one who switched and bought the duplex put nearly the same cash to work as a down payment, and now controls a $460,000 income-producing asset that pays them $20,000 to $30,000 a year and builds equity for them instead of for a landlord.

The salary bump from switching was never really the point. The point is that it got you to a down payment a couple of years sooner, and a couple of years sooner is the whole game when you’re compounding. The same $29,800 can sit in a savings account, or it can be the down payment on an asset many times its size that pays you to own it.

One caveat: I bought when I could lock a 3-4% 30-year fixed mortgage rate. Here in 2026, rates are higher, which makes the monthly payment meaningfully larger and the whole move harder to pull off right now. The principle still holds — switch for the higher income, save your 10% or more, and let an income-producing property carry most of the cost — you just have to run the numbers at today’s rates. Throughout, I’ve assumed savings earn 3% a year and inflation runs 2% a year, so a dollar of cash gains only about 1% in real buying power each year. These are illustrative figures to show how the pieces fit together, not a forecast or financial advice. Your market, interest rates, and the programs available to you will be different.

What You Should Actually Do

Switch when you hit the point of diminishing returns, usually 18 months to two years into a role. Not earlier—you need to deliver something, and you need the experience. Not later—the longer you stay, the staler you get and the less leverage you have to negotiate.

When you start looking, don’t undersell yourself. The outside market will almost always offer more than you think you’re worth. Companies have bigger pools of money for hiring than they do for internal raises.

And if your current employer makes a counter-offer? Usually that’s too little, too late. They’re reacting, not leading. The fact that it took you leaving to get them to budge is itself the data point. They weren’t planning to pay you that much while you stayed. And there’s an outside shot you’d be looking over your shoulder if you got a significant raise but continued in the exact same role.

The loyalty is to yourself: to your growth, your family’s financial security, and your actual market value. After all, you aren’t really working to increase the returns for shareholders, or contribute to a wealthy person’s second yacht/vacation home. You’re working is giving your time in return for compensation. And the company you work for, generally speaking, is looking at the arrangement just as simply- they pay you for the work you do. You aren’t “family,” you don’t owe them anything more than you offer them. Don’t let the opinions of family members from a different era, or peer pressure keep you from taking leaps and bounds- that isn’t a pathway out. That’s the path of the status quo.

The First-Property Bundle

The step-by-step playbook, the six-calculator deal-analyzer toolkit, and the down-payment-assistance finder — the exact system I used to go from a van to a duplex.

Pay what you want. Name your price — and if money’s tight, take it for less.

Get the bundle →Get the free $0-to-First-Property Roadmap

The five-stage plan I used to go from living in a van to owning a duplex, no rich parents required.