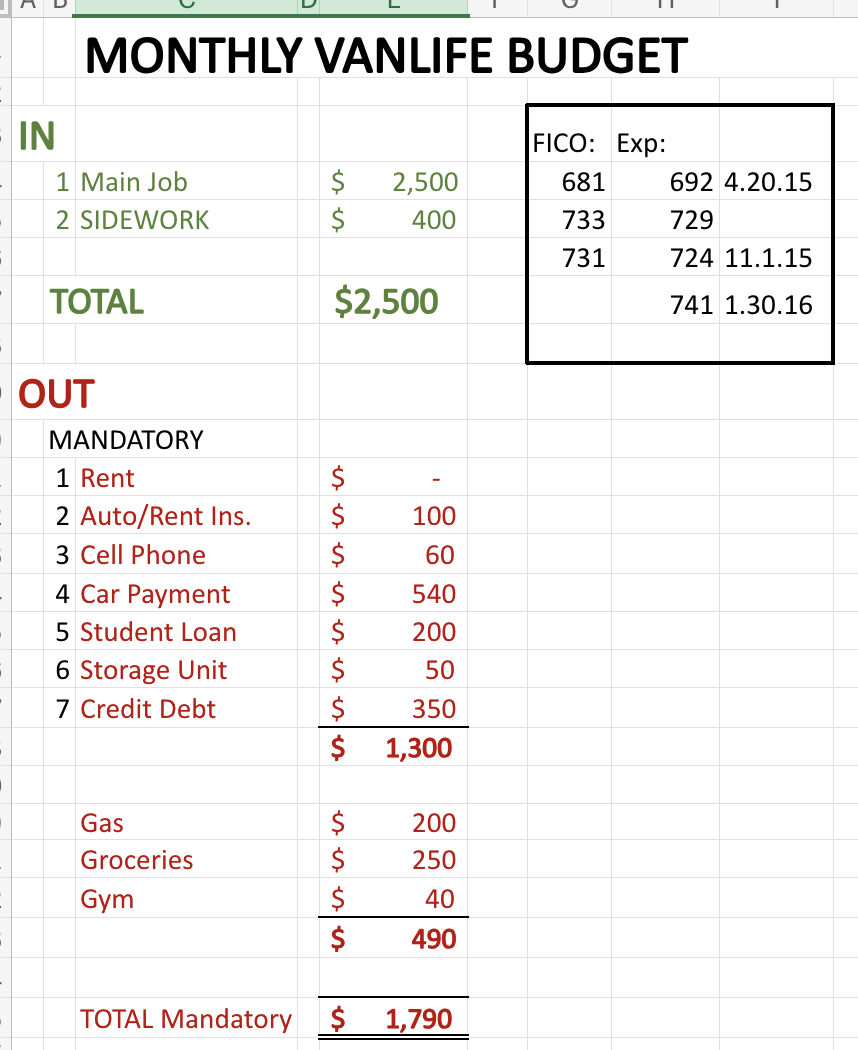

Step 1: I stopped paying for housing I couldn’t afford

The time spent living in a van or out of the back of a truck were not really lifestyle choices, I was housing-insecure (constantly changing places, multiple roommates, rented rooms, back at the parents off-and-on). But the brutal version of cutting my biggest expense to near zero did one thing: it stopped the bleeding. You cannot save a down payment while your rent eats every dollar. The first move is always to attack the biggest line in your budget, even if the answer is uncomfortable. I’m not telling you to live in a van. I’m telling you that housing is usually the line that decides whether saving is even possible, and most people refuse to touch it.Step 2: I moved where the math worked

In my old coastal city, a starter home cost about $700,000. In the Midwest, the same house cost about $200,000. Cost of living isn’t fixed, it’s a variable, and it’s the biggest one most people won’t change. Moving was hard. The spreadsheet was not ambiguous. If I stayed, I’d rent forever. If I moved, I’d own within a year.Step 3: I bought a small, unimpressive first house

My first place was a $185,000 starter home, under 700 square feet, built in the 1940s, nothing to photograph. With a modest down payment I could actually reach, it was mine. It wasn’t the dream. It was the launchpad.Step 4: I let that house build the next down payment

This is the quiet engine of the whole story. A few years later, the equity from that $185,000 house became the $16,450 down payment on a $470,000 duplex. I didn’t save the duplex down payment from my paycheck, a small, affordable purchase grew it for me. That’s the part nobody puts in a thumbnail: one modest house you can actually afford turns into the down payment on a bigger one. Repeat.What actually moved the needle

If I strip it down, four things did the work:- Killing the biggest expense (housing) instead of trimming small ones.

- Moving to where my dollars bought more.

- Buying small first instead of waiting for “the one.”

- Staying cheap longer than was fun while equity compounded.

Stuck on where to start? Tell me your situation. I’ve been at zero — actually below it.

Saving the down payment was just one piece — here’s the whole strategy it paid for.

Ready to go further?

The First-Property Bundle

The step-by-step playbook, the six-calculator deal-analyzer toolkit, and the down-payment-assistance finder — the exact system I used to go from a van to a duplex.

Pay what you want. Name your price — and if money’s tight, take it for less.

Get the bundle →Get the free $0-to-First-Property Roadmap

The five-stage plan I used to go from living in a van to owning a duplex, no rich parents required.