Real purchase price, real rent, real surprises. The numbers behind the house-hack you’ve read about in the abstract.

The hardest thing to find in real estate content is real numbers. Everyone talks in ranges and percentages and “your mileage may vary.” That’s understandable, every market is different, every deal is different, and a public-facing P&L is genuinely uncomfortable to write.

But it’s also the thing readers actually need. Vague advice rounds off to no advice. So here’s the receipt: my duplex. Purchase price, financing, rent, expenses, surprises, and what I’d do differently.

A few of these numbers are rounded for privacy, and one operating line (a normal year’s repairs) is a reasonable estimate rather than a penny-exact figure. None of them are made up.

The listing

I bought a side-by-side duplex in a working-class neighborhood in a midsize Midwestern city. Built in 1925, so nearly a century old, with all the character and all the deferred maintenance that implies. Two units, plus a finished basement with a separate entrance that the previous owner had been using as storage.

The property had been on the market for about 90 days. The previous owner was an out-of-state landlord who had managed it remotely and was, by his own admission, ready to be done with it. The upstairs unit had a tenant in place on a month-to-month lease, paying market-ish rent. The owner’s unit (which would become mine) was vacant.

A few things drew me in:

- It was priced for the market, not above it. Sellers who price their property accurately tend to be realistic in negotiations.

- The bones looked OK — on paper. I was told the roof had 8–12 years left and the boiler had been “reconditioned.” (Hold that thought. Both turned out to be optimistic.)

- The basement was a wildcard. Most buyers were probably looking at it as storage. I was looking at it as a third income unit if I could get it furnished and running as a short-term rental.

- The existing tenant paid on time. Confirmed via rent rolls and bank deposits.

The deal

Here are the numbers as they came together at closing, in 2021.

Purchase price: $470,000

Loan type: FHA (owner-occupied small multi)

Down payment: 3.5% = $16,450

Closing costs: $0 out of pocket, the seller covered them

Total cash to close: ~$16,450

This was actually my second home. I bought my first place, a tiny single-family starter home for $185,000, a few years earlier, and the equity from that sale funded this down payment. That’s the quiet engine of the whole journey: one modest, affordable purchase became the launchpad for a bigger one. (That starter-home story is its own post.)

Loan terms:

- 30-year fixed

- Interest rate: 3.125%, no points

- Base loan amount: $453,550

- Monthly principal and interest: ~$1,943

A note for the FHA nerds: FHA also charges a 1.75% upfront mortgage insurance premium (~$7,900 on this loan), which I financed into the balance rather than paying in cash. Folding that in nudges the real P&I up by about $34/month. I’m showing P&I on the base loan below for legibility.

PITI breakdown (monthly):

- Principal & interest: $1,943

- Property tax: $458 ($5,500/year)

- Insurance: $167 ($2,000/year)

- FHA MIP: $312

- Total monthly housing cost (PITI): ~$2,880

If you ran a property like this through the calculator, this is roughly what you’d see, these are the inputs that determined whether the deal was worth pursuing.

Getting operational

The existing upstairs tenant stayed on. I introduced myself, told them I’d be the new landlord, and walked their unit to look at any pending maintenance. Small move, big trust-building.

The basement project started early. The previous owner had treated it as storage. I confirmed the setup with the city, furnished it, and got it running as a short-term/midterm rental. Total upfront investment in the basement conversion: roughly $30,000, furniture, linens, kitchenware, a lockbox, supplies, and setup. (In hindsight this was high, and I’ll come back to it.)

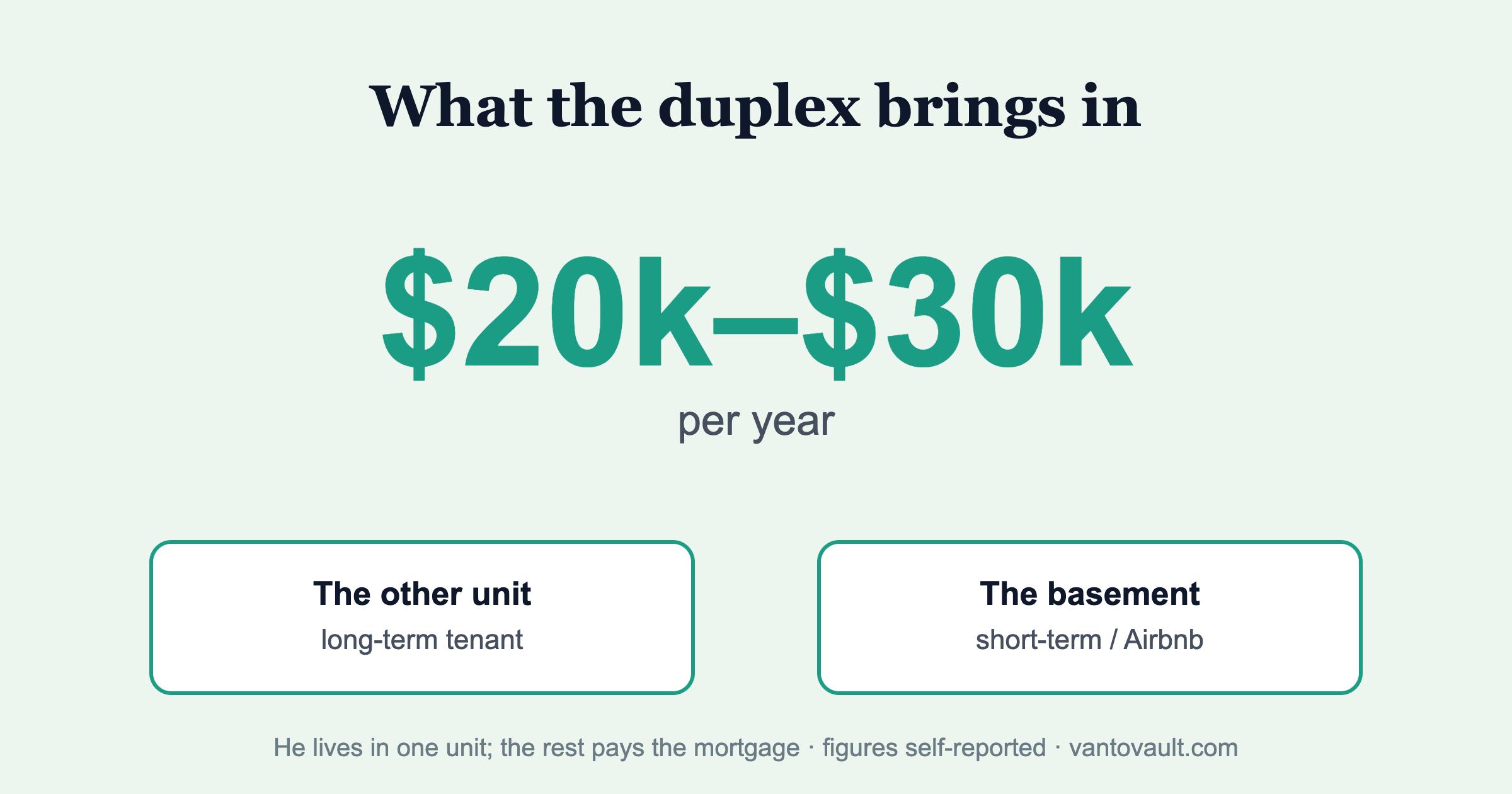

Once everything was running, here’s what the property collected each month while I lived in the owner unit:

- Upstairs tenant rent: $1,200/month

- Basement short-term rental: $11,000–$15,000/year net of platform fees, call it ~$1,083/month on average

- Owner unit (mine): $0 income, but my housing cost was now mostly covered

So while I’m living here, the property pulls in about $2,283/month, against my ~$2,880 PITI. That makes my effective housing cost roughly $597/month on the mortgage side, before utilities, which I’ll get to.

The expensive surprises (because of course there were)

If you buy a 1925 building and tell yourself you’ll get through ownership without surprises, you are setting up an unpleasant conversation with yourself. Mine didn’t all hit in month one, they showed up over the first few years, but they’re the real story, so here they are, in order of how much they stung.

Surprise #1: the boiler (year one). The seller had it “reconditioned” the year I bought, which sounded reassuring and turned out to mean “kept alive one more season.” It didn’t even make it through my first year, the original boiler had to be replaced outright. Cost: ~$20,000, in year one, right on top of the basement build-out. A reconditioned hundred-year-old heating system is still a hundred-year-old heating system.

Surprise #2: the chimney (year four). This one I didn’t see coming at all. Three years in, the chimney turned out to be structurally broken, quoted at ~$20,000 to properly repair. Rather than pour twenty grand into a chimney I didn’t strictly need, I had it safely closed off and capped for ~$5,000. Sometimes the right move isn’t to fix the thing; it’s to remove your dependence on it.

Surprise #3: the roof. I was told it had 8–12 years of life left. In reality it was closer to 30 years old — effectively at the end. Here’s the one lucky break in the bunch: a couple of years after I bought, a hailstorm did enough damage that insurance covered the replacement. I paid only my deductible. I’d love to claim foresight, but this was weather doing me a favor on a roof I’d have otherwise had to fund myself.

The lesson I keep relearning: if you’d run this property through the calculator with a 5% maintenance reserve, you’d have been badly short. Model maintenance high, 12–15% of rent, more on anything this old, and get your own trades to inspect the big systems, not just the general home inspector who flagged the boiler and roof as “fine.”

The full-year P&L

Here’s a representative stabilized operating year, rounded, while I’m living in the owner unit and self-managing. I’m showing a normal year on purpose: my literal first twelve months also absorbed the ~$30k basement build-out and the ~$20k boiler, so year one’s actual cash outlay was brutal and unrepresentative. The big one-time capital hits are deliberately not buried in the operating numbers below, smearing them into an “average” year would be exactly the kind of fuzzy math this site exists to call out.

Income:

- Upstairs tenant rent (12 months): $14,400

- Basement short-term rental (annual, net of platform fees): ~$13,000

- Total income: ~$27,400

Operating expenses:

- Property tax: $5,500

- Insurance: $2,000

- Utilities, I cover all of them for the entire building, my own unit included: ~$6,300

- Repairs & maintenance, normal year (estimated): ~$2,500

- Basement STR direct costs, cleaning, supplies, consumables: ~$1,000

- Property management: $0 (self-managed)

- Total operating expenses: ~$17,300

Net operating income (NOI): ~$10,100

Debt service (P&I, 12 months): ~$23,316

Pre-tax cash flow: ~ −$13,200

Total cash invested (down payment + basement setup): ~$46,450

Cash-on-cash return: ~ −28%

Now, before you close the tab, that negative number is the whole point, and it is not a bad deal. The property “loses” ~$13k a year on paper for one reason: I’m living in one of the units rent-free, so a third of the building produces no income. That’s not a leak; that’s the entire strategy. The house-hack arbitrage doesn’t show up in the property’s cash flow line. It shows up in my housing line.

The number that actually matters

Before the duplex, my housing cost was $1,500/month, the mortgage on that $185k starter home (and roughly what an equivalent rental would have run me).

After the duplex, my effective housing cost on the mortgage side is ~$600/month, because the tenants cover most of the payment. I do pay all the utilities for the building (~$6,300/year), but that figure already includes my own unit’s usage, which I’d be paying as any renter or owner anyway. The genuinely incremental cost of carrying the tenants’ utilities is only a slice of it. Even counting the whole thing, I’m housing myself for dramatically less than $1,500 a month while building equity on a $470,000 asset instead of a $185,000 one.

That’s the trade. A wildly “negative” property P&L, and a personal budget with hundreds of extra dollars in it every month and a much bigger asset compounding underneath me. If you only look at the property’s cash flow, you’ll talk yourself out of the best move available to you.

What I’d do differently

1. I’d budget the basement conversion more conservatively. I underestimated furniture costs and overestimated how fast bookings would ramp. If I’d modeled the basement at break-even for the first six months instead of profitable from the start, I’d have been more patient and made fewer impulse purchases. $30k was more than it needed to be.

2. I’d get the boiler and roof inspected by my own specialists, not just the general home inspector. The general inspector called the boiler “reconditioned” and the roof “8–12 years.” My own HVAC tech and a roofer would have told me the truth: one season of life left, and a roof that was actually 30 years old. That’s a $20k+ swing in how I’d have negotiated.

3. I’d build the tenant relationship from week one. My upstairs tenant turned out to be great, but I was too cautious early, treating them like a stranger instead of a long-term neighbor whose satisfaction is material to my financial life.

4. I’d model property management from day one, even though I don’t pay for it. The day I move out, that’s an 8–10% line item. Pretending it’s $0 forever gives you a misleading read on the property’s standalone economics.

What I got right

I bought a property whose math worked on conservative assumptions, not aggressive ones. I didn’t need a single basement booking for the deal to make sense as an owner-occupied house-hack. The basement was upside, not the thesis, which is exactly why the surprises hurt my pride more than my solvency.

I used FHA even though it meant permanent MIP. That $312/month of mortgage insurance is annoying, but the alternative was waiting years to save a 20% conventional down payment in a market that was appreciating faster than I could save. The MIP was the right trade.

I funded it with starter-home equity, not a windfall. There was no inheritance and no rich relative. A modest $185k house, bought when I could finally afford one, turned into the down payment on a $470k one. That’s the boring, repeatable mechanism nobody puts in a thumbnail.

I bought where the math worked, not where I most wanted to live. I’d still rather live back on the coast. But the math wouldn’t have worked there, and the math is what makes this site exist.

How to use this for your own deal

The point of showing my work isn’t to flex one deal, there’s nothing flex-worthy here. It’s a normal house-hack on a normal, century-old duplex with a broken chimney. The point is to give you a complete reference to hold up against your own numbers.

If you’re looking at a small multi right now:

- Run your listing through the calculator. If your projected cash flow looks much better than mine on similar assumptions, you’re probably missing an expense line.

- Model year-one with the surprises included. Add 1.5x your maintenance reserve. Old properties surface their problems early, and “reconditioned” is not a warranty.

- Run the long-term projection over a 5–10 year hold. A house-hack often looks unimpressive in year one and excellent in year five. That’s where it becomes legible.

- Reach out if you want a second pair of eyes. I won’t tell you whether to buy — that’s not my job. I’ll tell you whether your assumptions look reasonable, and where I’d push back if I were running the spreadsheet.

The companion post breaks down the eleven inputs and six outputs in more depth. If you’ve read this far, you’ll appreciate it.

Have a specific scenario you want me to run? Send it over. The more real listings I see, the more useful this site gets.

Get the free $0-to-First-Property Roadmap

The five-stage plan I used to go from living in a van to owning a duplex — no rich parents required. Enter your email and I’ll send it straight to your inbox.

Inside the place

The First-Property Bundle

The step-by-step playbook, the six-calculator deal-analyzer toolkit, and the down-payment-assistance finder — the exact system I used to go from a van to a duplex.

Pay what you want. Name your price — and if money’s tight, take it for less.

Get the bundle →Get the free $0-to-First-Property Roadmap

The five-stage plan I used to go from living in a van to owning a duplex, no rich parents required.